World Economic Outlook

World Economic Outlook Update, June 2020

June 2020

[$token_name="PublicationDisclaimer"]

A Crisis Like No Other, An Uncertain Recovery

Read full report PDF Download the Data

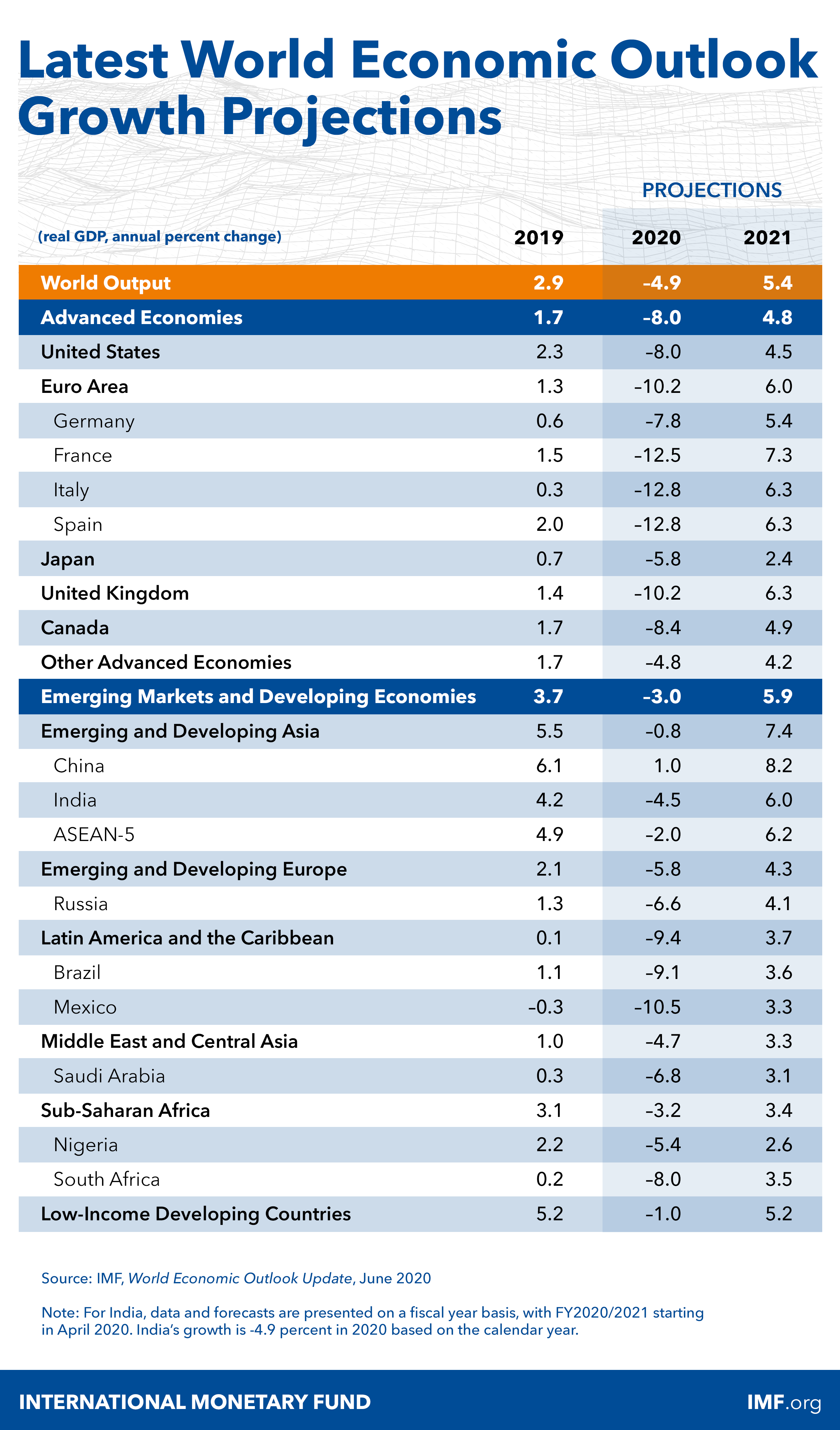

Global growth is projected at –4.9 percent in 2020, 1.9 percentage points below the April 2020 World Economic Outlook (WEO) forecast. The COVID-19 pandemic has had a more negative impact on activity in the first half of 2020 than anticipated, and the recovery is projected to be more gradual than previously forecast. In 2021 global growth is projected at 5.4 percent. Overall, this would leave 2021 GDP some 6½ percentage points lower than in the pre-COVID-19 projections of January 2020. The adverse impact on low-income households is particularly acute, imperiling the significant progress made in reducing extreme poverty in the world since the 1990s.

As with the April 2020 WEO projections, there is a higher-than-usual degree of uncertainty around this forecast. The baseline projection rests on key assumptions about the fallout from the pandemic. In economies with declining infection rates, the slower recovery path in the updated forecast reflects persistent social distancing into the second half of 2020; greater scarring (damage to supply potential) from the larger-than-anticipated hit to activity during the lockdown in the first and second quarters of 2020; and a hit to productivity as surviving businesses ramp up necessary workplace safety and hygiene practices. For economies struggling to control infection rates, a lengthier lockdown will inflict an additional toll on activity. Moreover, the forecast assumes that financial conditions—which have eased following the release of theApril 2020 WEO—will remain broadly at current levels. Alternative outcomes to those in the baseline are clearly possible, and not just because of how the pandemic is evolving. The extent of the recent rebound in financial market sentiment appears disconnected from shifts in underlying economic prospects—as the June 2020 Global Financial Stability Report (GFSR) Update discusses—raising the possibility that financial conditions may tighten more than assumed in the baseline.

All countries—including those that have seemingly passed peaks in infections—should ensure that their health care systems are adequately resourced. The international community must vastly step up its support of national initiatives, including through financial assistance to countries with limited health care capacity and channeling of funding for vaccine production as trials advance, so that adequate, affordable doses are quickly available to all countries. Where lockdowns are required, economic policy should continue to cushion household income losses with sizable, well-targeted measures as well as provide support to firms suffering the consequences of mandated restrictions on activity. Where economies are reopening, targeted support should be gradually unwound as the recovery gets underway, and policies should provide stimulus to lift demand and ease and incentivize the reallocation of resources away from sectors likely to emerge persistently smaller after the pandemic.

Strong multilateral cooperation remains essential on multiple fronts. Liquidity assistance is urgently needed for countries confronting health crises and external funding shortfalls, including through debt relief and financing through the global financial safety net. Beyond the pandemic, policymakers must cooperate to resolve trade and technology tensions that endanger an eventual recovery from the COVID-19 crisis. Furthermore, building on the record drop in greenhouse gas emissions during the pandemic, policymakers should both implement their climate change mitigation commitments and work together to scale up equitably designed carbon taxation or equivalent schemes. The global community must act now to avoid a repeat of this catastrophe by building global stockpiles of essential supplies and protective equipment, funding research and supporting public health systems, and putting in place effective modalities for delivering relief to the neediest.

Read full report PDF Download the Data